Control deals are gaining popularity because of the ability of the incoming controlling shareholder to control the ‘when’ and ‘how’ of the functioning of the business that is housed in the company. Additionally, the stigma associated with promoter’s relinquishing control of their companies is on the wane in India. Despite the market conditions, 2019 saw a fair deal of control transactions in the country. For such category of deals, calendar year 2019 was comparable to calendar year 2018 in number and value terms.

In this blog, we are sharing with you our analysis of control transactions in which exit was offered to public shareholders through the tender offer route in 2019[1], under the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (Takeover Regulations). We will be sharing a detailed report on the 2019 activity of such transactions separately.

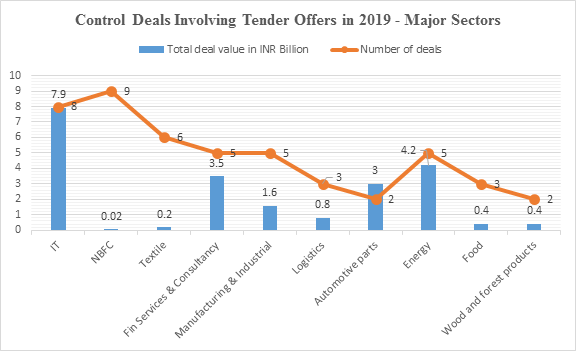

Between January and December 2019, the country witnessed as many as 61 tender offers. In terms of value, the technology sector saw the highest aggregate value of tender offers at INR 7.9 billion. In number terms, the non-banking financial companies (NBFC) sector continued to see the highest number of tender offers (nine in all). Other sectors that saw high activity were energy, services (including financial), automotive parts, logistics and manufacturing of industrial products.

In 2019, the five biggest tender offers by value were for Mindtree Limited (Technology sector), Adani Gas Limited (Energy sector), Reliance Nippon Asset Management Limited (Asset Management sector), WABCO India Limited (Automotive parts manufacturing sector) and NIIT Technologies Limited (Technology sector). These five offers comprised 79.62% of the aggregate value of all tender offers in 2019.

The following graph shows in number and value terms tender offers in major sectors in 2019:

2019 versus 2018

Below is a comparative snapshot of key trends of such control transactions for the years 2019 and 2018:

| 2019 | 2018 | |

| Number of tender offers | 61 | 70 |

| Completed tender offers (tender offers that were launched and completed in the same calendar year) | 39 | 49 |

| Number of Direct tender Offers | 58 | 63 |

| Number of Indirect tender Offers | 3 | 4 |

| Number of Tender Offers made due to breach of 5% creeping acquisition limit | 7 | 6 |

| Total value of tender offers | INR 226 Billion | INR 268 Billion |

| Number of tender offers for NBFCs | 9 | 12 |

| Number of tender offer where underlying transaction was closed before closure of the tender offer | 8 | 9 |

Other significant trends of 2019

- Busiest and slowest quarters: Q2 of 2019 was the busiest quarter for such control deals with 19 tender offers being announced. Q4 was the quietest with 12 tender offers being announced. Q2 of 2019 had the highest aggregate value of tender offers at INR 115 billion, while Q3 of 2019 witnessed the lowest aggregate value of tender offers at INR 7.8 billion.

- Foreign vs. Indian acquirers: Non-resident acquirers made 10 tender offers in 2019 at an aggregate value of INR 159 billion, which was 70.44% of the value of all tender offers in 2019;

- Control deals by financial investors: Certain financial investors made tender offers in 2019 to acquire control. These were Baring Asia’s tender offer for NIIT Technologies Limited (Technology sector), Blackstone’s tender offer for Essel Propack Limited (Packaging sector), Markab Capital’s tender offer for Uniply Industries Limited (Wood sector), Advent’s tender offer for DFM Foods Limited (Food sector) and Vista Equity Partners’ tender offer for Accelya Solutions India Limited (Logistics sector);

- Withdrawal: Tender offer for Upasana Finance, a NBFC, had to be withdrawn as the Reserve Bank of India did not approve the change in control; and

- Time taken by SEBI to clear: The average time taken by SEBI to issue its final observations on the draft letter of offer was 46 days. To issue its final observations, SEBI took anywhere between 15 days (in the case of Rapicut Carbides Limited and Yogya Enterprises Limited) and 98 days (in the case of Som Datt Finance Corporation Limited), which when compared to 2018 is significantly less.

The Year Ahead

Sectors that are likely to see a lot of M&A activity in 2020 (irrespective of whether it is a control deal) are energy, financial services, manufacturing, commercial real estate, technology (including e-commerce) and healthcare (including pharma).

*The authors were assisted by Principal Associate Gagan Sharma and Senior Associate Arnav Shah.

[1] Based on public announcements for open offers available on SEBI website as on January 3, 2020.

Related Article

-

Blog

BlogRegulatory Considerations for M&A Investors During COVID-19 Era

CAM authors collaborate for this article with our Guest Authors – Michael J. Cochran, Partner at Kilpatrick Townsend & Stockton and Gabrielle Gollomp , Associate at Dentons _ _ _ _ _ _ _ _ _ _ ...

28th September 2020 -

Blog

Control Premium: Analysis of Recent Top Deals and What 2020 is Likely to See

While of all us are getting used the to the new normal and are hoping that the worst will be behind us soon, we thought it would be great to share with you (i) our analysis of control premium paid in ...

9th April 2020