John Denver famously sang these lyrics in his famous love ballad, “Leaving on a Jet Plane”:

“’Cause I’m leavin’ on a jet plane

Don’t know when I’ll be back again

Oh babe, I hate to go”

When John sang these iconic words in 1966, when flying was quite the luxury, he could not even have dreamed how aptly they can be applied to the terrifying ‘Severe Acute Respiratory Syndrome Coronavirus-2’ (“COVID-19”) virus. With India going into a harsh and strictly enforced total lockdown from March end till May 17, 2020 (likely to be substantially extended), all airports have been shut and flights grounded. No one is going anywhere, whether they like it or not. No emotional love ballads will be sung, no jet planes will fly off into the sunset. A few repatriation flights have started to bring Indians stuck overseas back to India as part of the world’s largest peacetime repatriation effort, and allow some foreigners to leave India for their home countries – but as of now it is still a trickle.

But another thing may be worth singing ruefully about. With no one being allowed to leave India, COVID-19 has our Non-Resident Indians (“NRI”) in a tizzy over their tax residency. Given the severe flight restrictions in India and maybe their home countries as well, they are stuck in India, thus involuntarily increasing the time they have spent here. The excess period of stay in India may expose such individual’s offshore business and professional income to tax in India (which may be regarded as controlled from India and such individual regarded as a ‘Resident but Not Ordinarily resident in India’). Further, depending on the facts, if such individuals qualify as ordinarily Resident in India, then their global income could be exposed to tax in India.

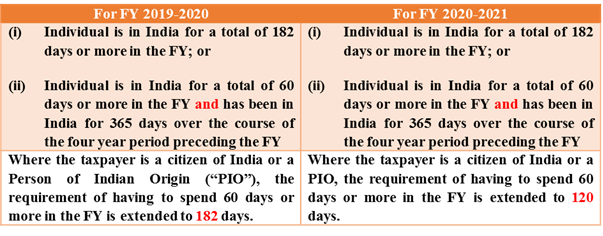

India’s Tax Residency Rules

The chart sets out India’s tax residency rules for the past financial year, ended March 31, 2020, and for the current financial year, which began on April 1, 2020 (as amended by the Finance Act, 2020):

Many high net worth individuals (“HNIs”) carry out substantial economic activities from India and plan their period of stay in India such that they remain a non-resident under the Indian Income Tax Act, 1961, and mitigate payment of tax on their global income in India. In fact, many such individuals maintain their affairs in a manner that they do not become residents of any tax jurisdiction and are not liable to tax in any country or jurisdiction. They are true global nomads, carefully choosing no country to really call “home”.

However, their involuntary stay in a country, owing to lockdowns and airports shutting, has spoilt this carefully choreographed dance across borders and rendered them tax resident of that country where they did not intend to maintain tax residence. Besides these HNIs, non-resident employees deputed to India and other NRI travellers, who are genuine tax residents of the countries in which they habitually reside and work, may face the risk of being treated as Indian tax residents. Some countries have brought back their citizens through evacuation flights, so the effect of the pandemic on the tax residence of such individuals can be expected to have been mitigated.

OECD Guidance

The Organization for Economic Development (“OECD”) published its guidelines on the matter in early April 2020,[1] advising that temporary dislocations on account of COVID-19 should not cause a concern over tax residence; and that in any event, a tax treaty between the jurisdictions in which the individual has potential residency will resolve conflict through the ‘tie-breaker’ test of residence (permanent home, habitual abode, centre of vital interests and nationality). The OECD guidance concludes by noting that since the COVID-19 crisis is a period of major changes and an exceptional circumstance, national tax administrations must consider a more normal period of time when assessing a person’s residence status. Unfortunately, OECD guidelines have little or no binding effect on national laws, much like any other instrument of international law, however their persuasive effect is incontrovertible.

Responses of USA, UK & Australia

In the days following the issue of the OECD guidelines, the US IRS provided for exclusion of up to 60 days from February 1 to April 1, 2020, for the computation of an individual’s residency under the local law’s ‘substantial presence test’. Even before the OECD guidelines were issued, the tax departments of the UK and Australia had come out with clarifications that are more liberal than the US notification. UK’s HRMC notified that it would accept days spent in the UK due to exceptional circumstances as a result of COVID-19 under certain scenarios. These scenarios include where an individual is quarantined or advised to self-isolate in the UK, advised by official government not to travel from the UK, unable to leave the UK because of international borders closing, or asked by their employer to return to the UK temporarily because of COVID-19. The notification clarifies that whether days spent in the UK can be disregarded due to exceptional circumstances will always depend on the facts and circumstances of each individual case. The Australian Taxation Office released guidance on the issue, highlighting that individuals who are in Australia temporarily due to COVID-19 will not become Australian tax residents if they usually live overseas permanently and intend to return there as soon as they are able to.

India’s response to forced residency

After intense pressure from affected taxpayers and global cues, India’s Central Board of Direct Taxes (“CBDT”) finally saw wisdom in addressing this issue. A notification[2] was released late on May 8, as per which the period of an individual’s stay in India between March 22, 2020 and March 31, 2020 (or the date of their leaving India on an evacuation flight before March 31, 2020) shall not be taken into account for determining tax residence. Additionally, where the individual was quarantined on or after March 1, 2020, he would be eligible to claim the period from the date of quarantine to March 31, 2020, towards the relaxation. This notification pertains only to financial year 2019-20 (or tax assessment year 2020-21). More clarity on relaxations for financial year 2020-21 is expected after lifting of the lockdown and resumption of international flights.

By way of example, Mr. Denver arrived in Bombay on September 22, 2019, and had made reservations to fly to Tokyo on March 22, 2020, just short of the requisite 182 days, but was unable to do so. His involuntary stay in India from March 22 to March 31 will not be counted towards determining his residence for the year 2019-20. He will remain a non-resident for income tax purposes for this financial year, despite overshooting his 182 day stay. Similarly, if Mr. Springsteen, who had also arrived with Mr. Denver, was evacuated to London, on April 15, his involuntary stay from March 22 to March 31 will not be counted towards determining his residence for the year 2019-20, and the 15 days of involuntary stay in the year 2020-21 will likely be discounted in accordance with CBDT directions, yet to be issued.

This comes as a major relief to many non-residents currently trapped in India, owing to the lockdown. However, there are still many cases that are not covered under the scope of the CDBT notification. E.g. many visitors may have cancelled their travel plans prior to March 22, not because they were quarantined, but simply because it may have been unsafe to travel abroad and risk exposure or certain death. Many individuals who live in mainland China or Hong Kong, and were visiting India just before the lockdown may be scared to travel back, given the severe quarantine restrictions and protocols put in place in those countries.

A better CDBT relief package should have been to extend the said notification beyond just the period of grounding of flights in India. The CBDT could consider taking a leaf out of the HRMC’s and the Australian Taxation Office’s books and waive off a broader stay period beginning from say, February, on a case-by-case basis. But at this stage, this appears ambitious and unlikely.

More CBDT clarifications on the issue are expected, for instance, on the scope of the term ‘quarantine’ – whether it covers self-quarantine sans advice by a health official – and whether any special cases that do not fall under the scope of the notification may be made out to tax assessing officers. Further, the interplay of the recent amendments to the residency rules via the Finance Act, 2020 (such as the concept of deemed residency and the introduction of a new monetary threshold of total income (excluding foreign source income) exceeding INR 1.5 million, on the basis of which minimum number of days of presence in India was reduced to 120 days) with COVID-19-related relaxations could lead to some unexpected complications. The Government has already announced that further relaxations to be issued upon resumption of international flights will exclude the period of stay of stranded individuals up to the date of normalisation of international flight operations. Till further clarifications come by, the May 8 notification is a step in the right direction to protect innocent NRIs from the draconian Indian tax machinery.

The COVID-19 situation has led to myriad combinations of residence conflicts and uncertainties for ‘global desis’ and nomads. One would do well to keep an eye out for these temporary relief measures from the CBDT, while collecting evidence to prove the intention to leave the country prior to the lockdown (should the CBDT permit case-by-case claims). Until then, stay home, stay safe and keep listening to John Denver.

[1] OECD Secretariat Analysis of Tax Treaties and the Impact of the COVID-19 Crisis, dated April 3rd, 2020.

[2] CBDT Circular No. 11/2020, dated May 8th, 2020 “Clarification in respect of residency under section 6 of the Income-tax Act, 1961”.

About the Authors

Rishabh Shroff

Partner (Co-Head - Private Client and Head - International Business Development)

rishabh.shroff@cyrilshroff.com Get in touchRelated Article

-

Blog

BlogRules for minimum remuneration notified for Indian managers of offshore funds to qualify for exemption from taxable presence in India

Background Section 9A of the Income-tax Act, 1961 (“IT Act”) carves out a special taxation regime to exempt eligible offshore funds from being regarded as having a business presence in India and h ...

5th June 2020 -

Blog

BlogIndian Tax measures to counter COVID-19 impact: How do they compare with OECD’s suggestions?

At a time when economic activities have come to a standstill on account of the lockdown imposed by the government to tackle the Covid-19 pandemic, some leeway in tax laws will provide much needed reli ...

22nd April 2020