The Finance Bill, 2020 (“Bill”) was presented as the Union Budget on February 1, 2020 (“Budget”) and then introduced in the Lower House of Parliament (Lok Sabha) – it was finally passed on March 23, 2020 with certain key amendments (“Amendment”). Interestingly, this was passed without any discussions in Parliament and received the presidential assent on March 27. Accordingly, the same will come into effect from April 1, 2020 (“Finance Act”).

The Finance Act needs to be seen in light of the ongoing COVID-19 pandemic being played out in India. As India undergoes a 21-day lockdown, post passing of the Amendment, the government is undertaking pro-active measures by way of press conferences to address the pressing needs of the society. To begin with, the government announced an extension of various statutory compliances for taxpayers (discussed below). Next, the Finance Minister (“FM”) announced a COVID-19 relief package for the poor, which primarily covers food security and direct cash transfers to them. Lastly, on March 27, Reserve Bank of India (“RBI”) Governor, Shaktikanta Das slashed the key lending rate by 75 basis points in an emergency move, to counter the economic fallout of the said lockdown. The RBI also permitted all commercial banks and lending institutions to allow a 3-month moratorium on loans. “Banks should do all they can to keep credit flowing,” Mr Das said.

These are extremely helpful and proactive steps being taken by the government and RBI. The private sector keenly awaits a suitable stimulus package, if any, in line with what is playing out in USA, Canada, etc.

Meanwhile, the Union Budget’s emphasis on wealth creation is unlikely to be fulfilled, given the havoc wreaked by COVID-19 on economic stability of India and around the globe. Most of the Budget’s proposals focussed on increased scrutiny of High Net-worth Individuals (“HNIs”) and Non-resident Indians (“NRIs”). For instance, the proposals on residency rules in India and the taxation being levied based on the same, widened the scope of Indian tax net and did not come as a relief in any form to the HNIs or NRIs.

Following the proposals in the Budget, the government received feedback / representations from various stakeholders, including revision or clarification of many provisions therein. The government appears to have taken some of the said representations into consideration while making the Amendment and passing the Bill.

The following are the key changes being made to the Bill by way of the Amendment:

KEY CHANGES

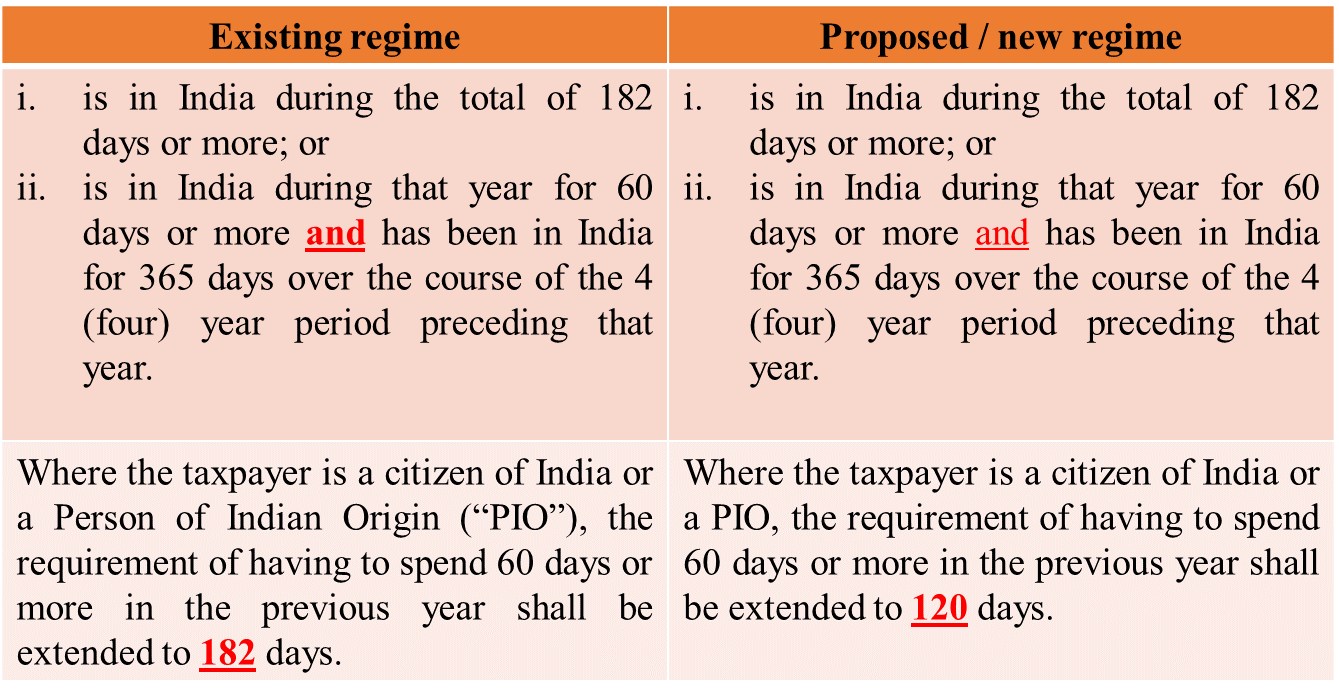

- Changes to residency rules of citizens or PIOs:

In India, tax is levied basis the residence of a taxpayer and the source of income. An Indian resident is taxed on their worldwide income while a non-resident would only be subject to tax on income accruing from India.

The Income Tax Act, 1961 (“IT Act”) specifies certain tests to determine tax residency. The Act states that an individual would be a resident in India in the previous year, if he:

This was introduced due to the fact that many Indian HNIs had been taking advantage of the provision to carry on substantial economic activities within India, without qualifying as residents in India. Thus, pursuant to the Budget, any citizen of India or a PIO who has been resident in India during that year for 120 (one hundred and twenty) days of more and has been in India for a total of 365 (three hundred and sixty five) days over the course of the 4 (four) year period preceding that year would qualify as an Indian tax resident and be subject to tax in India on their worldwide income.

However, by way of relief, the government has clarified through the Amendment that the reduced 120 (one hundred and twenty) days criteria will be applicable only to those Indian citizens or PIOs, whose total income (excluding foreign source income) exceeds INR 1.5 million. For this provision, income from foreign sources means income which accrues or arises outside India (except income derived from a business controlled in or a profession set up in India). This comes as a relief to NRIs and PIOs whose India-sourced income is less than INR 1.5 million, while others should continue to re-examine their period of stay in India.

- Tax based on citizenship:

Through the Budget, the government proposed to add a new section to the IT Act which provides that an Indian citizen shall be deemed to be an Indian tax resident if he/she is not liable to tax in any other country by reason of domicile or residency or any other criteria of similar nature, regardless of whether such individual meets the residency test laid out above. Further, a Press Release was issued by the Central Board of Direct Taxation (“CBDT”) dated February 2, 2020, which had clarified that any person who qualifies as an Indian resident pursuant to the proposed amendment would only be subject to tax in India on their income which has been derived by them from an Indian business or profession.

The Finance Bill has now been amended to provide that the proposed deemed resident provisions will apply only to those Indian citizens whose total income (excluding foreign source income) exceeds INR 1.5 million.

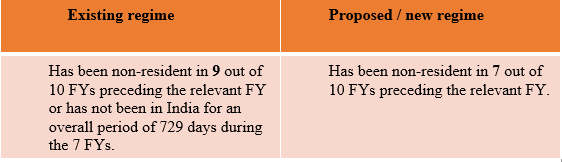

- Further relaxations to Residents Not-Ordinarily Resident in India:

The IT Act currently provides that an individual or an HUF would be treated as a ‘not ordinarily resident’ of India in the relevant financial year (“FY”), if such a person:

Such persons would not be subject to tax in India on their worldwide income but only on their income arising out of India. These proposals were set forth to take effect from April 1, 2020. However, the Finance Act has scrapped the said relaxation entirely.

Further, based on the changes proposed, i.e. if an Indian citizen or a PIO becomes a resident of India upon exceeding a 120 (one hundred and twenty) day stay in India or an Indian citizen is deemed to be a resident in India as he/she is not liable to be taxed in any other country (as discussed above), it is now been clarified that such persons would qualify to be a ‘not ordinarily resident’ of India.

The Finance Act, by deleting the said relaxation of 7 (seven) years which, was sought to be introduced earlier, has taken away the only ray of sunshine for NRIs. The change in the Budget came as a major relief to Indians who needed the flexibility to take a decision of staying back in India on or returning to countries outside India. However, as can be noted from the various new proposals, the government’s intent to scrutinise Indian HNIs and NRIs continues. Thus, extremely careful planning may be required for NRIs who either frequently visit India or who has income arising out of various sources in India.

- Clarifications in relation to the abolition of the Dividend Distribution Tax

The Budget had proposed to abolish the Dividend Distribution Tax (“DDT”) and sought to tax dividends at the hands of the respective shareholders. The said changes are proposed to be effective from April 1, 2020. However, the changes being introduced by the Budget left scope for various ambiguities, including the applicable tax rate to non-residents. Please see our detailed analysis in relation to the changes and clarifications being provided through the Finance Act, here: http://tax.cyrilamarchandblogs.com/2020/03/provisions-for-taxing-dividend-income-receive-yet-another-upgrade/

- Relaxing the scope of Tax Collection at Source

The existing provisions of the IT Act provide for a mechanism for Tax Collection at Source (“TCS”) on businesses such as trading in alcohol, forest produce, scrap, etc. The Budget had expanded the scope of TCS provisions to transactions such as the foreign remittance under Liberalised Remittance Scheme (“LRS”) subject to a minimum threshold of INR 700,000 in an FY for remittance out of India. Any amount exceeding the said threshold shall be chargeable at 5% TCS.

The Amendment states the changes will be effective from October 1, 2020. Further, it clarified that the exemption threshold would not be applicable to amounts being remitted for purchasing an overseas tour package. Further for LRS remittances of an education loan obtained from a financial institution, the government has relaxed the TCS rate from 5% to 0.5%.

RELAXING COMPLIANCE OBLIGATIONS

Based on representations from various stakeholders, the government has decided to extend the last day of filing income tax returns for FY 2018-19, which is otherwise March 31, as well as the deadline for filing Goods and Services Tax (“GST”) returns, which needs to be done on a monthly basis until June 30, 2020.

Accordingly, at the PC, the FM stated the following:

- For delayed payments of taxes, interest will be levied at a reduced rate of 9% instead of 12%;

- For delayed deposit of TDS for the current FY, interest will be charged at a reduced rate of 9% until June 30, 2020. The FM, however, stated that there shall be no extension to this deadline;

- Deadline for linking of Aadhaar and PAN shall also be extended to June 30, 2020;

- The Vivad se Vishwas tax dispute resolution scheme introduced by way of the Budget, will be extended by three months to June 30, 2020. Those availing the scheme under the extended deadline will not have to pay 10% interest on the principal amount.

The FM concluded the PC by stating that there would be more announcements to look out for in this regard including that of an economic package for those industries affected by the pandemic. Though the FM has not hinted at any time, such a package, when announced, will bring some cheer to India Inc. The positive impact of USA’s USD 2 trillion stimulus package, introduced on March 24, can already be seen on the stock markets of many countries. On March 25, the stock markets of India, Japan and Australia made a strong recovery.

CONCLUSION

The government’s objective of respecting India’s wealth creators, as seen from the Economic Survey and the FM’s Budget speech, was perceived as a nod towards the possibility of introducing significant promoter-friendly policies. However, the actual proposals in the Budget did not move towards this goal; and in fact increased the scrutiny and taxability of such wealth creators. The Finance Act, thus, comes as a relief to NRIs who have been working abroad and frequently visit India. While there have been no major reversals of the Budget proposals, these new changes shed some light on to the fate of the Indian HNIs and UHNIs.

However, the government’s primary focus, like all major countries at the moment, is on fighting the pandemic and prescribing stringent safety measures to curb the spread of the pandemic. Not to mention, to stabilize the economic shock of the pandemic. It may not be unreasonable to expect further economic measures, relaxations, stimuli etc. in the coming days to ease the shock. In our opinion, the Budget was passed in light of a very different economic scenario and it will have to be periodically refined to factor in the pandemic. The bedrock of the Indian economy is its family businesses, and they will need to be resilient in these times.

Due to the increasing complexity of the tax regime and the various options being provided to each taxpayer under the old and new regime, careful planning and approaching your attorney should be your top priority to avoid getting blindsided by an expensive tax bill. Further, in light of the revised deadlines being announced by the FM, it is best to approach your attorney at the earliest, for advice on any change in your tax filings that may need to be undertaken basis the above.

The threat of the pandemic is too real now to be ignored any further. As is being stated by the officials in Italy, ignoring the issue in the beginning has resulted in its current situation. Planning and early implementation is crucial. As we prepare to take all the necessary measures to protect ourselves, it is also important to ensure that your assets remain safeguarded and you remain in good health and spirits.

About the Authors

Rishabh Shroff

Partner (Co-Head - Private Client and Head - International Business Development)

rishabh.shroff@cyrilshroff.com Get in touchRelated Article

-

Blog

BlogRegulatory Considerations for M&A Investors During COVID-19 Era

CAM authors collaborate for this article with our Guest Authors – Michael J. Cochran, Partner at Kilpatrick Townsend & Stockton and Gabrielle Gollomp , Associate at Dentons _ _ _ _ _ _ _ _ _ _ ...

28th September 2020 -

Blog

Covid-19: Bumpy roads ahead for Highway Sector

The Covid-19 pandemic has affected the society in an unanticipated and unprecedented way. To contain its spread, the Ministry of Home Affairs (MHA), Government of India vide its order dated March 24, ...

2nd July 2020