As you are aware, the Finance Minister, Ms. Nirmala Sitharaman, presented the Union Budget 2020-2021 on February 1, 2020 and consequently, introduced the Finance Bill, 2020 (“Bill”) in the Lok Sabha. The Bill comprised the financial proposals, including taxation related proposals, to amend the provisions of the Income-tax Act, 1961 (“Income-tax Act”) for the financial year 2021. Subsequently, the Finance Minister and her team had several discussions with various stakeholders, who we understand made many representations, seeking changes in some of the proposals. Pursuant to this, amendments to the Bill were presented and the Bill, incorporating the amendments was passed by the parliament on March 26, 2020 and received the assent of the President of India on March 27, 2020. It has now been enacted as the Finance Act, 2020 (“Finance Act”).

The Income-tax Act comprised provisions in relation to the taxability of, and exemptions available to, infrastructure investment trusts (“InvITs”) and real estate investment trusts (“REITs”, together with “InvITs”, referred to as “business trusts”) registered with the Securities and Exchange Board of India under the Securities Exchange Board of India (Infrastructure Investment Trusts) Regulations, 2014 (“InvIT Regulations”) or the Securities Exchange Board of India (Real Estate Investment Trusts) Regulations, 2014 (“REIT Regulations”), respectively.

The following are the proposed changes in the Bill, in relation to taxability and exemptions available to business trusts in India:

-

Change in the definition of ‘business trusts’:

A `business trust’ was defined under Section 2(13A) of the Income-tax Act to mean a trust registered as an InvIT under the InvIT Regulations or a REIT under the REIT Regulations, units of which, are required to be listed on a recognised stock exchange in accordance with the InvIT Regulations or REIT Regulations, as the case may be.

The Finance Act has amended the definition of `business trusts’ which earlier recognised only listed InvITs and REITs registered with SEBI to now include unlisted InvITs registered with SEBI as well. This amendment will take effect from April 1, 2020.

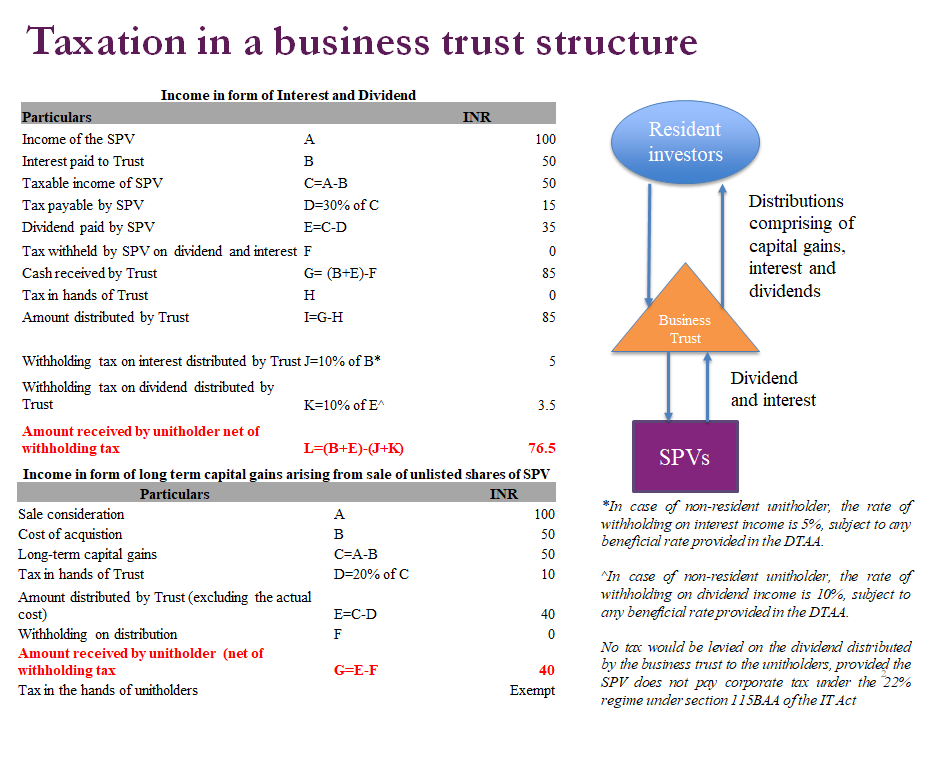

Capital gains realised on the transfer of units of unlisted private InvITs shall be taxable at the rate of 10% (plus applicable surcharge and cess) in hands of a non-resident unitholder and 20% (plus applicable surcharge and cess) for resident unit holder, provided the units have been held for more than 36 months. The short term capital gains (where units have been held for less than or equal to 36 months) will be taxed at the rate of 30% (plus applicable surcharge and cess) for residents and 40% (plus applicable surcharge and cess) for non-resident corporates. Non-resident unitholders may claim the beneficial provision available under the applicable double tax avoidance agreement (“DTAA”), if any. Long term capital gains arising from market sale of listed units, both in the hands of residents and non-residents, are taxed at the rate of 10% (plus applicable surcharge and cess) on gains exceeding ` 0.1 million while short-term capital gains will be taxed at the rate of 15% (plus applicable surcharge and cess).

-

Dividend Distribution Tax replaced with Dividend Withholding Tax:

Under the erstwhile Section 115-O of the Income-tax Act, dividend distributed by a domestic company was subject to dividend distribution tax (“DDT”), in the hands of the company, at an effective rate of 20.56% (including surcharge and cess). Such dividends were generally exempt in the hands of the non-resident unitholders in India though they may have been taxable in the home jurisdiction of a non-resident unitholder. Further, as per erstwhile Section 115-O of the Income-tax Act, dividend distributed by a special purpose vehicle (“SPV”), in which a business trust held the entire share capital other than as required to be held by the Government or any regulatory authority, was exempt from DDT. The dividend received by business trusts from their SPVs was then distributed to the unitholders without any further tax being levied on it.

The Finance Act has abolished the DDT regime as applicable to companies and has shifted the incidence of taxation of dividend on the shareholder or unitholders. Accordingly, as per the amended provisions, (i) dividend income would be subject to tax in the hands of the shareholders, at the applicable rate; and (ii) the SPV would be required to withhold tax on the same. However, the business trust will continue to be exempt from tax on dividend income from an SPV. Since no mechanism for an SPV to not withhold tax from dividends, when distributing to business trust, is not provided, the business trust may have to provide a nil withholding tax certificate to the SPV to ensure that no tax is withheld by the SPV while distributing dividend to the business trust.

Further, the business trust would now be required to withhold tax on the distribution where the income being distributed is in the nature of dividend income received from the SPV, as described below:

a. Taxation of dividends at the Business Trust Level:

The erstwhile Section 10(23FC) of the Income-tax Act exempted certain income of business trust being, (i) interest income received from an SPV, where the business trust held controlling interest and such percentage holding prescribed under the InvIT Regulations or REIT Regulations; and (ii) dividend income from an SPV in which the business trust held the entire share capital other than as required to be held by the Government or any regulatory authority.

The Finance Act has made no changes in respect of the taxation of interest income of a business trust. However, it has exempted the dividend income received by a business trust from an SPV, in which the business trust holds controlling interest or such percentage holding under the InvIT Regulations or REIT Regulations as may be prescribed. This amendment shall come into effect from April 1, 2020.

Subject to any capital gains tax that may be applicable, the total income of a business trust (other than interest and dividend) shall continue to be charged to tax at the maximum marginal rate of 42.7%.

b. Taxation of dividends at the Unitholder level:

Erstwhile Section 10(23FD) of the Income-tax Act provided that any distributed income, received by a unitholder from the business trust, other than interest income or rental income (i.e. rental income earned directly by a REIT) would be exempt from the total income of the unitholder. The Bill had proposed that in addition to interest income and rental income, dividend income distributed by the business trust to the unitholders, would also be subject to taxation in the hands of the unitholders with effect from April 1, 2020. Accordingly, interest and dividend income distributed to unitholders were proposed to be taxed at the tax rates applicable to each of the unitholders.

The Bill also proposed that dividend income received by residents and non-resident unitholders would be subject to withholding tax at the rate of 10%. However, in case of non-residents, any lower rate as may be provided in the DTAA between India and the country of residence of the non-resident unitholder may be applicable, provided such non-resident is eligible for the benefits available in the DTAA provisions.

This tax on dividend in hands of unitholders is seen to be as a less favourable tax treatment under the new tax regime for dividend, as compared to the DDT regime. However, the Finance Act has provided some concessions. Now the amended the Income-tax Act provides that dividend distributed by abusiness trust shall be exempt in the hands of the unitholders, provided the SPV distributing the dividends has not exercised the option to pay corporate tax under the 22% corporate tax regime available in terms of, and subject to compliance with, Section 115BAA of the Income-tax Act. The corresponding withholding tax provisions have also been amended.

These amendments will take effect from April 1, 2020.

-

Taxation of interest and rental income on unit holders of a business trust:

In terms of Section 194(LBA)(1) of the Income-tax Act, any distributable income in the nature of interest income and rental income in the hands of a resident investor is subject to deduction of tax at the rate of 10%. Similarly in terms of Section 194(LBA)(2) of the Income-tax Act, any distributable income in the nature of interest income and rental income in the hands of a non-resident is subject to deduction of tax at the rate of 5%. No change is proposed in the Bill in respect of taxation of unitholders on interest and rental income received from the business trust.

-

Applicability of DDT in a multi-level business trust structure

In terms of the InvIT Regulations and the REIT Regulations, an InvIT or a REIT is permitted to have a multi-level holding structure, being one where the business trust holds shares in the SPV through a holding company (“Multi-level Structure”). It would be relevant to note that the erstwhile Section 115-O of the Income-tax Act did not exempt a Multi-level structure from the applicability of DDT. Accordingly, dividend paid by an SPV to its holding company was subject to DDT at an effective rate of 20.56% (inclusive of surcharge and cess). The Bill which abolished Section 115-O of the Income-tax Act, had proposed to reintroduce Section 80-M in the Income-tax Act. This section provides for a deduction for dividends received by one domestic company from another domestic company, limited to the amount of dividend received from the investee company if the shareholder company pays dividend before the specified due date. Thus, under the provisions of the Bill, the holding company would be able to claim deduction for the dividends received from the SPV, resulting in avoidance of double tax on dividends. The Finance Act, in addition to confirming the aforementioned proposals, has further extended the deduction under Section 80-M of the Income-tax Act to dividends received from business trusts and foreign companies. Accordingly, as per the new provisions, a unitholder of the business trust which is a domestic company, may claim a deduction for the dividends received by it from a business trust, subject to conditions provided under Section 80-M of the Income-tax Act.

A comparison of taxation in the hands of an investor who invests in a business trust structure versus in the shares of a holding company structure, where in both cases the income stream comes from the underlying SPV, which would be helpful in deciphering the changed provisions:

Related Article

-

Blog

Provisions for taxing dividend income, receive yet another upgrade

The Finance Bill, 2020 (the “Bill”) was recently passed by the Lok Sabha (Lower house of the Parliament) on March 23, 2020, with more than 50 amendments to the Bill. The Bill has now received the ...

30th March 2020 -

Blog

BlogDividend Distribution Tax Abolishment: Here’s Something Lost in Translation

The government has said taxes on income received from dividends will now have to be paid by the shareholders instead of the dividend distributing company. The Finance Bill 2020 presented alongside the ...

17th February 2020